MH Advantage

Manufactured homes offer upgraded features with MH Advantage. What’s a manufactured home?

Unlike a traditional site-built home, a manufactured home is constructed at an indoor facility using efficient building processes. These manufactured homes are built on a permanent chassis, or frame, and are delivered and installed at your chosen home site on land you either own or rent. Manufactured homes can closely resemble traditional site-built homes, but often cost less.

A special mortgage for manufactured homes

MH Advantage® is a mortgage product designed specifically for innovative manufactured homes with the appearance and features of traditional site-built homes — including garages, modern kitchens and bathrooms, energy-efficient appliances, covered porches, high-quality exterior siding, and more — which allow them to blend into any neighborhood.

Benefits of an MH Advantage mortgage

To be eligible for an MH Advantage mortgage, your manufactured home must be located on land you own and used as a principal residence or second home — not an investment property. Here are some of the benefits:

- Allows for 30-year fixed-rate financing.

- Down payment as low as 3%.

- Potentially lower interest rates compared to other manufactured home financing.

- Flexibility to fund down payment and closing costs from multiple sources, including gifts and eligible grants.

- Opportunity to cancel mortgage insurance once your home equity reaches 20%.

Getting a MH Advantage mortgage

1. Work with your lender to see if you qualify for an MH Advantage mortgage.

2. Visit a manufactured home retailer and ask about MH Advantage-qualifying features.

3. Select and customize your manufactured home with the relevant features.

4. Have the home delivered and installed at the chosen site.

5. Close the mortgage loan and move in.

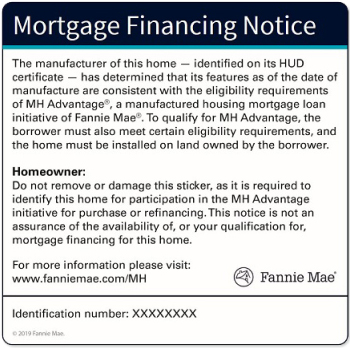

The MH Advantage sticker — like the one shown here — is usually placed in a discreet location in the home, such as a utility closet or a cabinet under the kitchen sink. The sticker is extremely important, as it identifies a home as meeting the standards for an MH Advantage mortgage, so don’t remove it. Doing so could prevent the home from qualifying for MH Advantage financing if it’s refinanced or sold in the future.

More to explore

What You Need to Know About Home Loan Basics

Ready to apply for a mortgage? Start here to learn some basic home loan terms and the lender's role.

Get to Know the Types of Mortgage Loans

Choose the best home loan for your needs by learning about common loan types such as fixed-rate, adjustable-rate, FHA, USDA, and VA loans.

How to Choose a Lender

An important step in homebuying is finding the right lender. Use this guide to find the right one for you - which could result in lower costs over the life of your loan.